Few things are as exhilarating as starting a new business. Whether you want to diversify your income with a side hustle or leave a lasting impact, starting your own business is an enticing path forward.

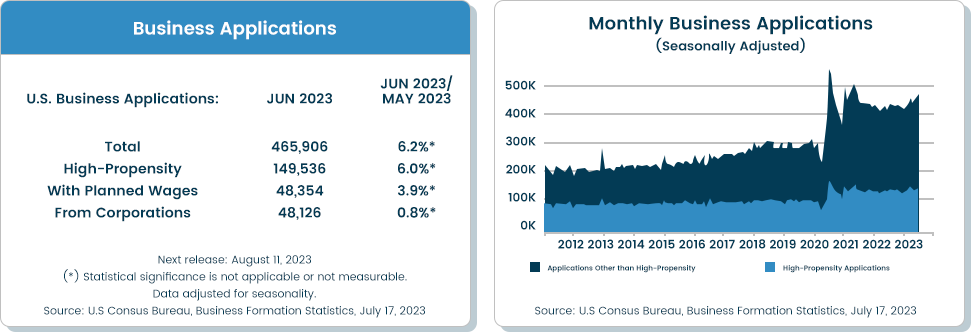

But before you take the self-employment plunge, it’s important to note that an entrepreneur’s life can be filled with challenges and setbacks. And with more than 465,000 new business applications filed in June alone, be prepared to face fierce competition.

When considering entrepreneurship, and considering a drastic change in lifestyle, take some time to process some key statistics so that you can begin to craft your step-by-step approach to overcoming common challenges. Seven to ten percent of small business startups shut down every year and the figures climbed to 23 percent during the COVID-19 pandemic.

That makes it crucial for aspiring and new entrepreneurs to tread with caution. Here are a few helpful tips for starting your own business and finding a path to success.

Outline your business plan

One of the most common mistakes new entrepreneurs make is to start a business without a concrete business plan. Moving forward without a plan could set your business up for failure.

Creating a comprehensive business plan requires a lot of hard work, but comes in handy at various stages, such as when approaching investors for funding or searching for ideas to scale operations. It should define various aspects of your business, including your business idea, target market, structure, growth strategy, anticipated start-up costs, your mission, and vision.

Start by identifying a niche and defining your business idea. Determine whether you can build a profitable business model with this idea. Identify and analyse potential competitors to get an insight into market demand and begin to map out the kind of business you’d like to own.

Use questionnaires, focus groups, and surveys to understand if your product or service will attract enough paying customers in your target demographic. It’s also a good time to decide on a business name and set your short-term goals and long-term vision.

Next, decide on the legal structure you want to set up for your business. You can choose one of the following business structures:

- Sole proprietorship

- Partnership

- Corporation (S-Corp or C-Corp)

- Limited liability company (LLC)

The type of business entity you choose influences various factors, such as your personal liability and the taxes you must pay.

Don’t forget your license, registration, and insurance

Business registration is a crucial step to launching your business legally. You have to get it registered with the secretary of state. Besides legal registration, you’ll also need to obtain an employer identification number from the IRS.

Next, it’s time to get business licenses and permits to conduct your business operations. The specific permits you need will depend on your business structure, industry, and location. You must also open a business bank account and likely apply for business credit.

While you’re at it, make sure you get adequate business insurance coverage. The most common type of coverage small business owners use is general liability insurance. It protects your business against claims of workplace injury, personal injury, and property damage.

Depending on your niche and target market, you can also opt for additional coverage, such as:

- Product liability insurance

- Media liability insurance

- Business continuity insurance

- Worker’s compensation insurance

Focus on financial planning

Whether starting an online business like a dropshipping apparel business or a professional services firm, you need adequate working capital. This is critical for conducting market research, developing new products/services, attracting potential customers, and building your brand.

Before you meet potential investors, you must outline a solid financial plan. It’ll give you a clear idea of immediate and long-term expenses and how much money you’ll need to break even.

If your finances permit, bootstrapping your business ensures complete ownership and gives you more control over business operations. However, if bootstrapping isn’t an option, you can secure funding from angel investors and venture capital firms. Alternatively, you can opt for small business loans or grants to avoid early equity dilution. You can also use crowdfunding platforms like Kickstarter to invite others to invest.

Getting funding is only the first step in financial planning. You also need a well-defined cash-flow management strategy to make the most of business finances.

Prioritise product development

Your product or service has to stand out from the crowd. Otherwise, you’ll likely struggle to attract and retain customers.

Start by analysing competitors’ products to find ways to set your business apart. Next, define your target customer base and segment your target market to determine each group’s needs, preferences, and pain points. The key is to refine and tailor your offerings for each market segment.

It’s worth noting that product development is an ongoing process. You must refine your offerings and introduce new features based on customer feedback. Conduct surveys and monitor customer service requests to identify areas of improvement.

Build your marketing and branding strategies

You need a consistent and memorable brand identity to outshine your competitors. Define a clear brand persona and use it to design your company’s logo, website, social media assets, business cards, brochures, and other promotional materials.

Build a robust search engine optimisation (SEO) strategy to establish and improve your website’s online visibility. Use tools like Semrush and Ahrefs to identify your target keywords. Then, use these keywords to create high-quality, personalised content for each customer segment.

Whatever your niche, it’s crucial to develop an omnichannel marketing plan and strengthen your online presence with social media marketing, content marketing and if feasible, paid advertising. Identify the social media platforms your target audience is most likely to use and publish enriching, relevant, and valuable content on these platforms to build a loyal audience.

Define a customer acquisition strategy

The right marketing campaigns can help you grab eyeballs. But to build a successful business, you must outline a concrete sales pipeline that qualifies, nurtures, and converts leads. In other words, identify and optimise various touchpoints a prospect goes through before purchasing your product.

Email marketing can come in handy here. Use automated drip email campaigns to take each lead on a personalised buying journey.

A robust customer relationship management (CRM) platform can give your sales team a detailed overview of each prospect and customer. Use it to monitor where each lead stands in the sales pipeline and devise ways to move them forward.

A CRM solution like Act! CRM with built-in marketing automation can be instrumental in attracting and retaining customers. With Act!, you can segment mailing lists, set up automated response-based email campaigns, and streamline lead nurturing.

Streamline operations with technology

Launching and growing a business can be simplified using modern tech-driven solutions. For instance, you can use project management software to facilitate employee collaboration and communication—a particularly helpful feature for dealing with a hybrid workforce.

Similarly, accounting software like Quickbooks can streamline bookkeeping and eliminate human errors. You can also use tools to automate various business functions, including HR, payroll, and marketing.

Besides leveraging automation, you can outsource specific tasks to third-party vendors or freelancers. This can improve efficiency and give you more time to focus on scaling your business.

Develop your skills

As an entrepreneur, you need more than business acumen and technical expertise to build a successful business. You must develop and polish a broad spectrum of skills, from negotiation and networking to problem-solving, budgeting, and strategic thinking. You need managerial and leadership skills, too.

While you should be passionate about growing your business, it’s also crucial to prioritise work-life balance. Burnout will interfere with your ability to lead and inspire your team and achieve your goals. Know when and how much to delegate to your employees, if you have them, and seek support and guidance from other business owners in your network or members of the small business administration (SBA).

Start your own business the right way

Now that you know how to start your own business, you must be eager to begin your journey. But before you do, take the time to outline your business plan and growth strategy. Also, make sure you have a clear idea of how you’ll promote your offerings and attract customers. Lastly, embrace the right tech to straighten your path to scaling up.

A CRM and marketing automation solution can be a powerful ally for new business owners. Click here to try Act! for free and learn how it can fit into your business.