Managing customer risks with Act! Premium

Simply said, if you are a financial advisor, insurance agent, or providing other financial professional services, your book of business is always in peril. Silent erosion, split relationships, the cost of getting the wrong customers, and managing customer infidelity are all ongoing concerns.

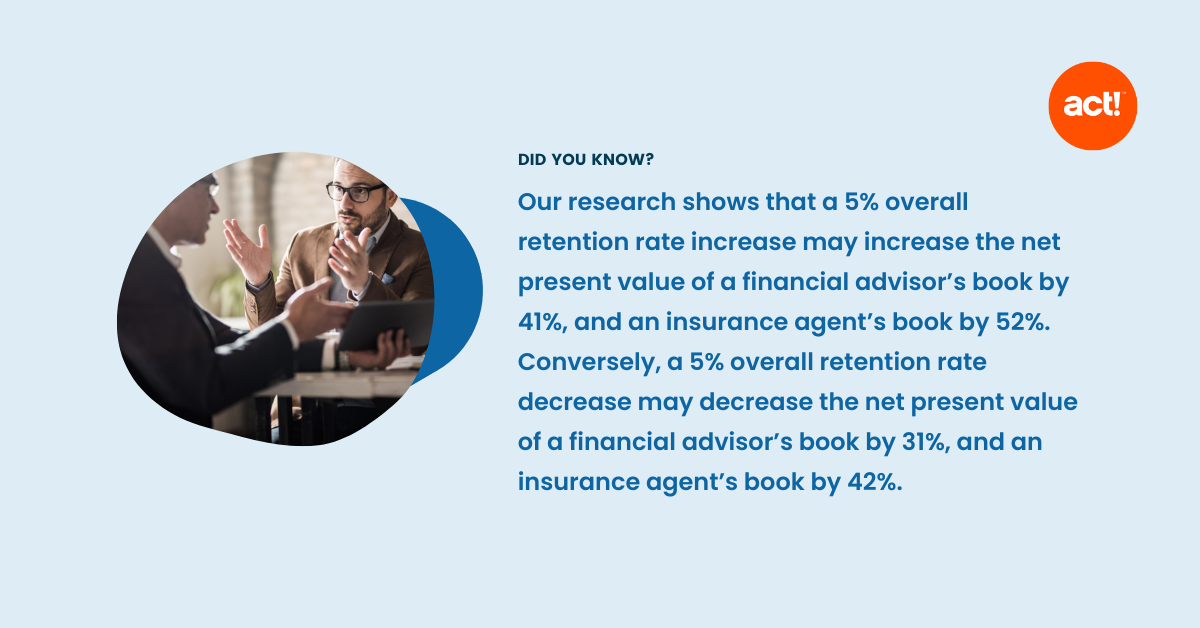

Every financial professional wants to optimise their book’s annual gross revenues, net present value, and future cash flows. The ultimate exit value of their book of business is related to a multiple of annual gross revenues and future cash flows. The multiple is dependent on:

- Probability of customer retention

- Depth of customer relationships (share-of-wallet)

- Customer characteristics (age, income, net worth, location)

- Historical trending and stack ranking of customer fee income

It’s important to know that many book-of-business risks can go unnoticed, and yet be deadly to your business. The financial results and ultimately sale value of any book of business are driven by three risks:

- Retention Risk

- Growth and Penetration Risk

- Acquisition Risk & The Cost of Getting The Wrong Customers

Risk Summary

Retention Risk – Keeping customers for life & the cost of “Silent Erosion”

The cost and frustration of customer acquisition are high, so the longer you are able to keep a customer, the more you can spread the cost. Additionally, the cost to replace a lost customer is also high so the longer the life of a relationship, the higher the net present value of your book.

Financial advisors often say that retention is not a problem, yet when we distinguish retention of share of wallet, or your share of the customer’s total business, we find that while financial advisors haven’t totally lost a customer, they may have lost much of their business to other financial advisors. This is the definition of ‘silent erosion’.

Growth and Penetration Risk – Managing ‘Customer Infidelity’

There is always the risk that someone else will grow your customers. And, ‘split connections’ means customers are making financial and investment decisions every day. If you are a financial advisor, and your customers have abandoned old 401K plans at past employers, and investments with banks, insurance agencies, and other advisors, numerous parties are potentially managing your customers’ financial portfolios.

Why are financial relationships so fragmented? I believe “customer buying patterns directly reflect an advisor’s selling patterns”.

Growth risk is real – in terms of both missed opportunities (life events) and customer defection due to poor service delivery or inferior portfolio performance. The goal is penetration and consolidation (share-of-wallet) of the relationship.

Acquisition Risk – The cost of getting the wrong customers & subsidising unprofitable customers

As long as the emphasis is on volume (a common practice at larger firms and wirehouses), financial advisors will go after the short-term, easy hits because all sales lead to revenue volume, profitable or not, high service cost or not, and sustainable or not. This course of least resistance is not always the best course – but it is the easiest one.

We must think of new customer acquisition cost as a scarce resource, like capital, and ask the question, “what prospecting effort will give the greatest return?” If you could make only one prospect call next year, are you clear on what the profile would look like? Just because you have customer referrals or easy access to prospects does not mean those prospects should be at the top of your list. If you get only those that you seek out, you may be displeased to discover that you got what none of your competitors wanted.

Act! Premium – Helping financial advisors manage customer risks and grow their book of business

Most financial advisors (and insurance agents) are trying to manage more than 200 customers in their book of business – nearly an impossible job without the help of a CRM like Act Premium, which has been designed to enhance customer acquisition, growth, and retention.

Referral management

It is vitally important to stay in touch with your customers and let them know you are accepting new clients. Ask for referrals and invite your customers to ‘bring-a-friend’ events. Act! Premium’s e-marketing capabilities can be configured for automated and scheduled emails. The email messaging can be scheduled and customised for different customers and automated for delivery on specific dates.

Life events & analytics (predictive and propensity)

Life events (a new birth, marriage, divorce, death, inheritance, graduation, a new home, a change of residence, a change in employment, retirement, etc.) usually trigger financial decisions. Life events can be revealed in a digital questionnaire every six months. The questionnaire can be automatically sent by Act! Premium’s e-marketing capabilities and timed just before a semi-annual customer review. The questionnaire responses can be automatically entered into Act! Premium’s customer record with a notification to the financial advisor (and a digital brochure to your customer). The Act! Premium system has predictive analytics (growth and retention alerts) and propensity models (my other clients like you – age, income, risk tolerance, etc. – are investing in . . .) to help you manage your book of business.

The metrics that matter

Your book is your most important Asset Under Management (AUM) – and you should manage it like it is an asset. Track key performance metrics (KPIs) – insights to make better decisions related to acquisition, growth, and retention. All these KPIs increase your book valuation. Act! Premium tracks and reports on the following KPIs.

- AUM trending (growth and retention) and stack ranking

- Retention rates (along with trending and stack ranking)

- Probability of customer retention

- Best referral sources

- Book value (and net present value)

- Depth of customer relationships (and share-of-wallet)

- Customer characteristics (age, income, net worth, location)

- Fee income (historical customer fee income trending and stack ranking)

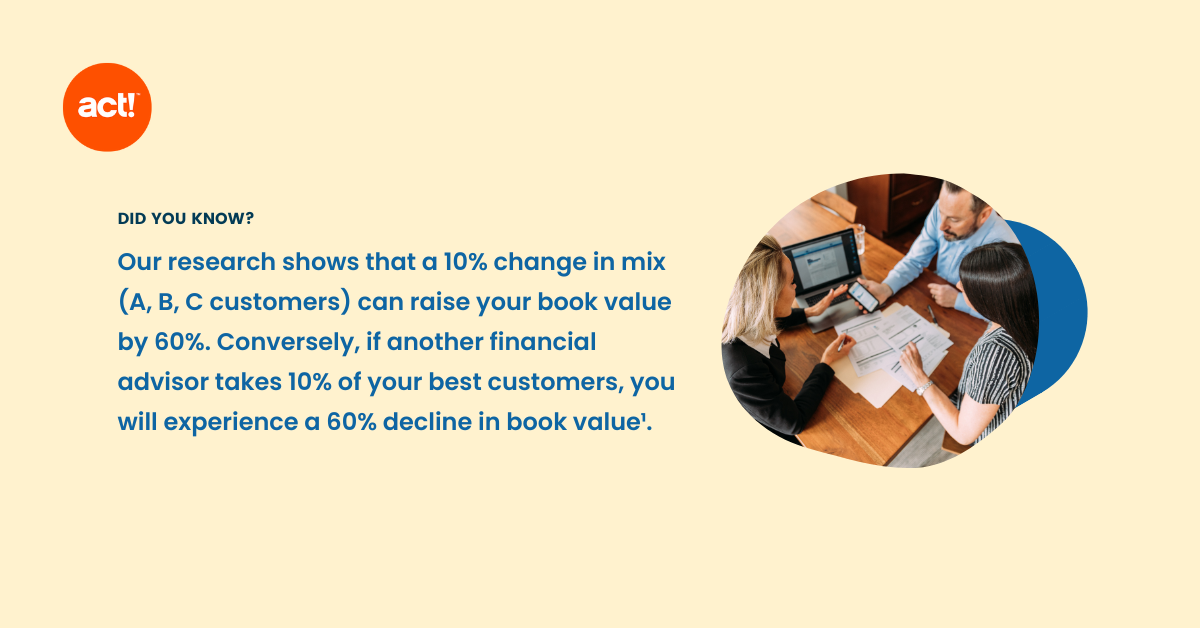

- A, B, C segmentation along with the change of mix and impact on book value.

- Share of wallet (AUM/net worth) trending

Retention alerts & analytics

Act! Premium is constantly analysing your book for signs of ‘silent erosion’ and sending you alerts.

Sales reports, dashboards & analytics

Act! Premium sales reports and dashboards are visual, interactive, and cascaded from the financial advisor to the CEO. Act! Premium sales reports and dashboards use data from the entire sales stack.

- A Daily (and YTD) Portfolio SNAPSHOT

- Interactive Pipeline Reports

- Stack Ranking & Trending Reports

- Book-of-Business Dashboards

- Customer Dashboard

- Prospecting & Lead Generation Reports

- Fee Income & Incentive Compensation Reports

- Coaching Dashboard & Linked Reports

- Referral & Life Event Dashboard & Linked Reports

- Investment Reports & Analytics

- E-Marketing Reports & Campaign Dashboards

- Aging Reports

- Customer Service SLA Reports & Dashboards

- Team Leaderboards

For more information and a demo

Let us show you how Act! Premium can be your sales assistant to quickly increase your retention rates, change your customer mix, generate referrals and life event leads, manage more customers with less effort and improve your book valuation.

About the author

Ron Buck is the Chairman & CEO of Performance Insights – an industry-leading software company serving the financial services industry. Ron is a recognized industry leader and has taken two companies public prior to Performance Insights.